BDC RISK Profiles

BDC RISK PROFILES

Quality of credit platform and management, exposure to retail, oil/commodities, CLOs, historical credit performance, NAV stability/growth, reaching for yield and dividend coverage

The following information is to help investors properly assesses relative risk for BDCs in order to value investments in a sector that is notoriously opaque. BDC stock prices can be volatile providing opportunities for investors that have identified proper values based on risk and potential dividend returns. Assessing relative risk and dividend coverage are primarily responsible for driving a wide range of values for BDCs. It is important to realize that BDCs do not report consistently, so investors need to look beyond changes to net asset value (“NAV”) per share and dividend coverage from reported net investment income (“NII”).

Risk Rankings

After performing the analysis discussed below on each BDC, I assign a risk rank from 1 to 10 with 10 implying the safest. The rankings are focused on capital preservation Net asset value (“NAV”) per share stability as well as portfolio strength to sustain dividend coverage. This includes the ability for the portfolio to retain value during an economic downturn and/or rising interest rates. Both of these scenarios could put pressure on cash flows of portfolio companies and the ability to support debt and interest payments.

I mostly cover higher quality BDCs with the exception of a few (mostly for comparative reasons to establish a range including pricing) as well as companies with higher trading volumes and liquidity which can be an advantage when trying to buy and sell shares as well as overall volatility. SUNS, FDUS, and MRCC are the most thinly traded BDCs that I actively cover.

Assessing Risk for BDCs

The following are some of the methods that I use for comparing risk profiles among BDCs:

- Quality of management

- Portfolio credit quality: vintage analysis, concentration issues, etc.

- Exposure to higher risk sectors, structured products (CLOs and SLPs), subordinated debt

- The amount of “true first-lien” loans

- Strong dividend coverage versus “reaching for yield”

- Stable versus declining NAV per share

- Access to capital: current leverage, SBIC availability, ability to issue equity

- Fee structures and conflicts of interest versus internally managed

- Inside and institutional ownership

Portfolio Credit Quality

One of the best approaches to assessing risk in a BDC portfolio is using a “vintage analysis” that takes into account many things including the time frame that each loan was originated as well as asset class, maturity, directly originated vs. syndicated, sector, PIK, and cash yields. Most likely, BDCs that were lending during times of less protective covenants and higher leverage multiples while maintaining higher-than-average yields were making riskier loans at the time.

Assessing which vintages are potentially riskier than others is an evolving art and there are few key indicators that I use including historical market liquidity levels, default rates, leverage multiples, and covenant light trends. More importantly, I compare the cash and PIK yields of each loan by the time frame that they were originated but also taking into account the asset class and company sector. Specifically, I am looking for “above market” yields that could imply higher risk. Another important indicator is loans that should have been refinanced at lower rates and are past their “prepayment penalty” windows. This would include loans that have much higher than current market yields and could easily be refinanced unless the portfolio company has potential credit issues. After going through this analysis each quarter, there is a clear trend with riskier vintages and ongoing or upcoming credit issues. Many of the BDCs that I have considered to have higher risk portfolios are already experiencing credit issues, but there are a few that could worsen.

Not All First-Lien is Equal

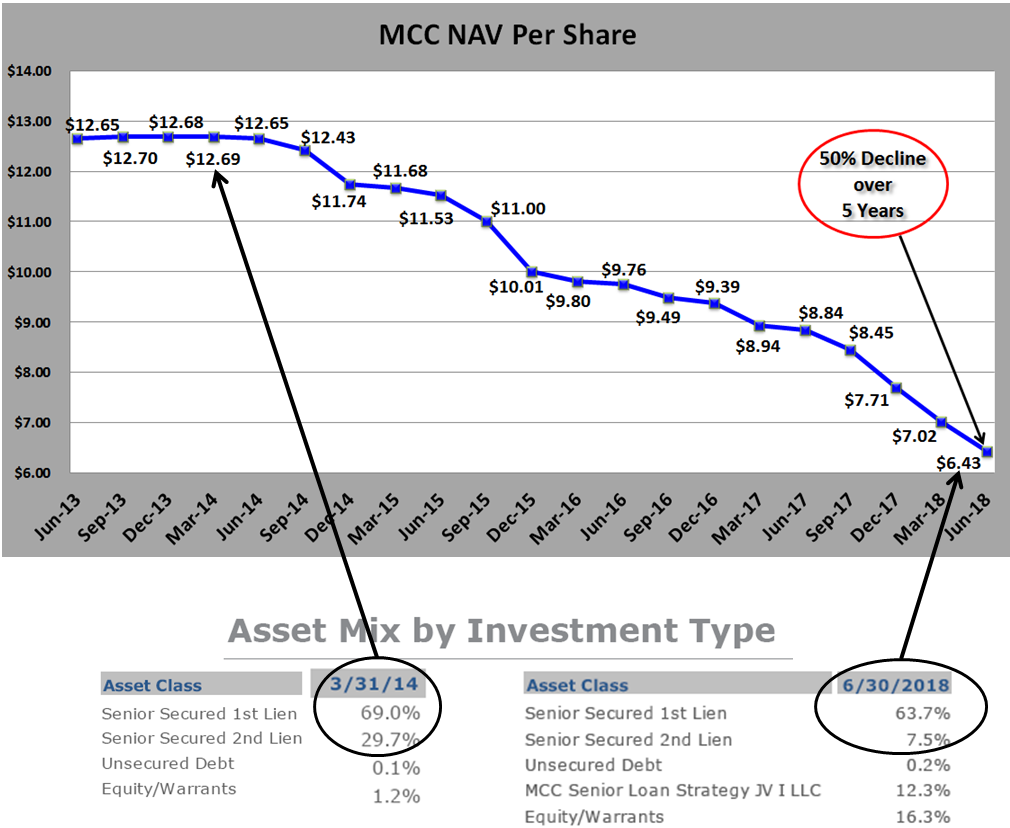

As mentioned in previous articles, Medley Capital (MCC) grew the portfolio at potentially riskier periods and is an example that not all BDCs with large amounts of first-lien debt are necessarily ‘safer’ than others. Before the recent credit issues, MCC had a portfolio of almost 70% senior secured first-lien debt, that is still around 65%, but over the last 5 years, declining credit quality has resulted in four dividend cuts and a 50% decline in NAV per share as shown in the chart below.

Strong dividend coverage versus “reaching for yield”

Another key factor is the need to “reach for yield” to sustain the current dividend. Some BDCs are actively rotating the portfolio into higher yield investments that typically involve more risk. Many BDCs have been experiencing increased credit issues and others could begin to see additional non-accruals in the coming quarters.

BDCs that can safely cover dividends during worst case and lower yield scenarios have many advantages over other BDCs including being more selective with investments. This could include only investing in higher credit quality companies with lower leverage multiples, having stronger protective covenants and taking a higher position in the capital structure. This is what I refer to as “true first-lien”.

Please see Dividend Coverage Levels for more information.

Stable versus declining NAV

Changes in NAV per share are not always a clear indicator of historical credit issues because there are many items that impact NAV including over or underpaying the dividend, equity issuances and general changes in values for assets and liabilities (borrowing facilities). It is also important to recognize the difference between “realized” and “unrealized” gains and losses. BDCs that have recently cut dividends due to credit issues likely had larger amounts of realized losses from investments sold or written off. Many higher quality BDCs have had previous NAV per share declines mostly related to unrealized losses and marking assets down to reflect general market pricing rather than actual changes to credit quality.

Assessing the quality of management

This is likely the most important part of BDC analysis as management is responsible for building a portfolio to deliver returns to shareholders while protecting the capital invested. BDC management controls all the levers including the quality of the origination/credit platform, managing the capital structure with appropriate leverage, meaningful share repurchases, accretive equity offerings and dividend policy, creating an efficient operating cost structure and willingness to “do the right thing” by waiving management fees or having a best in class fee structure that protects returns to shareholders. Many of the indicators previously discussed are directly tied to the quality of management including:

- Portfolio credit quality driving stable versus declining NAV

- Dividend increases versus decreases over the last two years

- Reaching for yield

- ‘Total return’ features included in management incentive fee structures

- Insider ownership

- Previous management trust issues

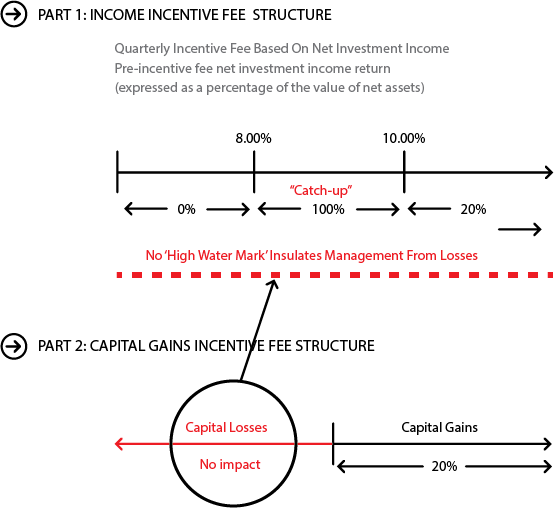

Fee structures and conflicts of interest versus internally managed

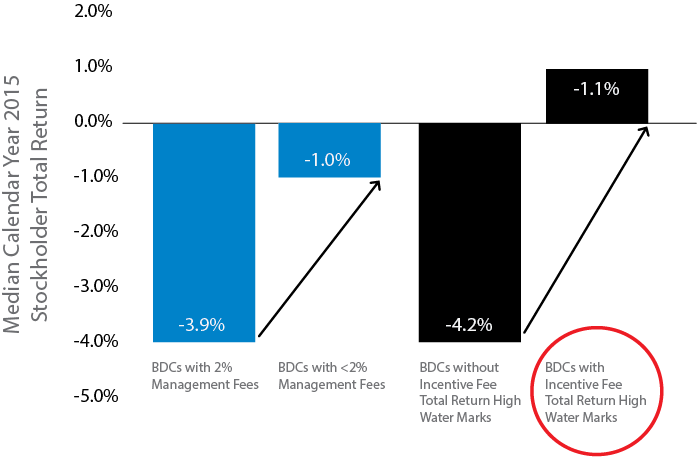

The older incentive fee structures can incentivize management to take on increased risk with investors’ capital. Management benefits from higher yields (through higher income incentive fees) with less risk related to future credit issues because capital losses are not included when calculating income incentive fees. This could lead to management taking higher risks (for increased yields) due to being insulated from potential capital losses when calculating the income portion of the incentive fees. Ultimately, management could receive higher fees during periods of declining NAV per share, resulting in lower total returns to shareholders.

The following chart is from FS Investment Corp (FSIC):

2015 STOCKHOLDER TOTAL RETURN PERFORMANCE

DEMONSTRATES THAT FEE STRUCTURES MATTER